Fintech in China

It's bad. We just don't understand why it has to be so bad.

We're cracking down on a Chinese proxy buyer who has been extensively abusing our loyalty system—Pawprint Powerplay. The guy really has some balls, and they made us do it for the first time ever, as we have traditionally been very tolerant of proxy buyers.

Unlike most scenarios we've seen where customers appoint a third-party forwarder to save on shipping costs (since we've sold to over 80 countries and there are many we're not specialized in regarding logistics), most of our Chinese friends seeking help from a third party are doing so not for logistical purposes, but rather for payment.

China has its unique payment ecology (if not unique in everything). Credit/debit cards are rarely used as a method of payment, even though China has its widely accepted credit card standard, Union Pay (we accept that, too), and almost every personal bank account in China is associated with a Union Pay debit card by default. In fact, most Chinese people don't even know their bank account number; instead, they refer to the Union Pay card number of that associated debit card. Union Pay provides a robust system allowing you to instantly send money to another account using its Union Pay card number, and it is supported by every bank. Most importantly, it's free for personal accounts (though not in the old days, which we'll talk about). The U.S. equivalent, Zelle, was founded in 2016, and Union Pay had already done the same thing at least a decade before that.

While it all sounds like a perfect and fabulous system (like most of the big projects in China), a key factor you shouldn't ignore is that most banks in China are either state-owned or have strong government backgrounds. They're naturally stiff-necked and don't give a shit about customer experience at all. Although they had a fancy Union Pay system, they used to charge people significant amounts (comparatively, given China's economic situation at that time) for sending money between banks. Some companies would rather withdraw cash (in millions) from one bank and then walk it to another to save the monstrous fees.

This offered a great opportunity to Alipay, originally a copycat of PayPal, since it was developed as the payment gateway of Taobao, a copycat of eBay (everybody knows the relationship between PayPal and eBay, right?). Alipay, like PayPal, enables you to store money in your account and transfer money among accounts. Most importantly, it's free. This broke the dominance of Chinese banks and eventually pushed them to reduce fees and improve customer service, but people, hating their service, embraced Alipay, and by the 2010s it became the de facto standard of mobile pay and small-amount transfers. WeChat, the dominant IM app in China, later introduced WeChat Pay and has been competing with Alipay in a duopoly.

So, although Union Pay has a great and modern system that combines credit cards and bank accounts, enabling both payments and money transfers in an easy and low-cost way, the banks just ruined it and gave all the market to Alipay and WeChat. They also stopped making products better. Union Pay debit cards and most credit cards don't support CVC + billing address authentication by default, and they are only usable on websites specially designed to authenticate PIN codes (usually through an ActiveX plugin, which will be your nightmare).

And that is why our Chinese friends couldn't easily place orders with us, even though we're sure that 99% of them have a Union Pay card on hand.

So, why don't we just allow people to pay with Alipay? That is what this long article is all about. We feel like it's a good opportunity to honor our tradition of transparency, as we can't ignore some angry fans attributing this to our arrogance (or even worse, discrimination). Honestly, we don't blame them, since they might think it's a super easy, click-and-go thing. But they should be ready for the truth.

We began looking into Alipay a long time ago, but back then, there were only some shabby third-party providers connecting their own Alipay gateways to your Shopify store, and you had to withdraw the money directly from them. Finally, in 2025, we noticed that Alibaba (the company that owns Alipay) introduced their official platform, Antom, aimed at serving overseas merchants who want to accept Alipay payments. They have their own official Shopify app, too.

We began with the standard onboard procedure. Everything looked fine. A few days after the initial application we were informed that they need some additional documents from us. And here's how the thing began to get fancy.

We all know that Alibaba is an online retail company that likes to pretend to be a 'tech' company, but you would expect a leading "tech" company in China to have the basic ability to put up a simple, functional website. No, they can't. This entire Antom website is a showcase of noob software engineering failures.

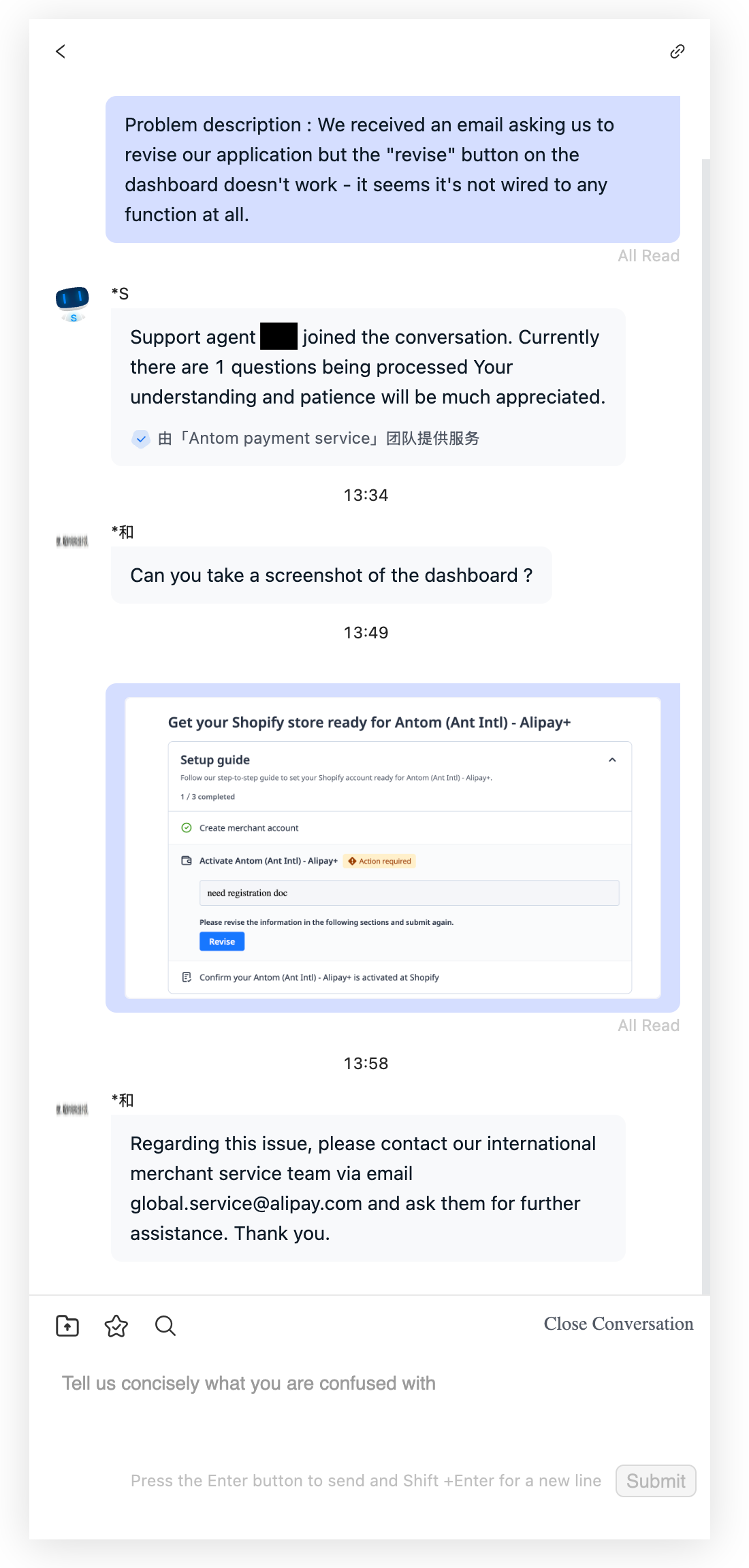

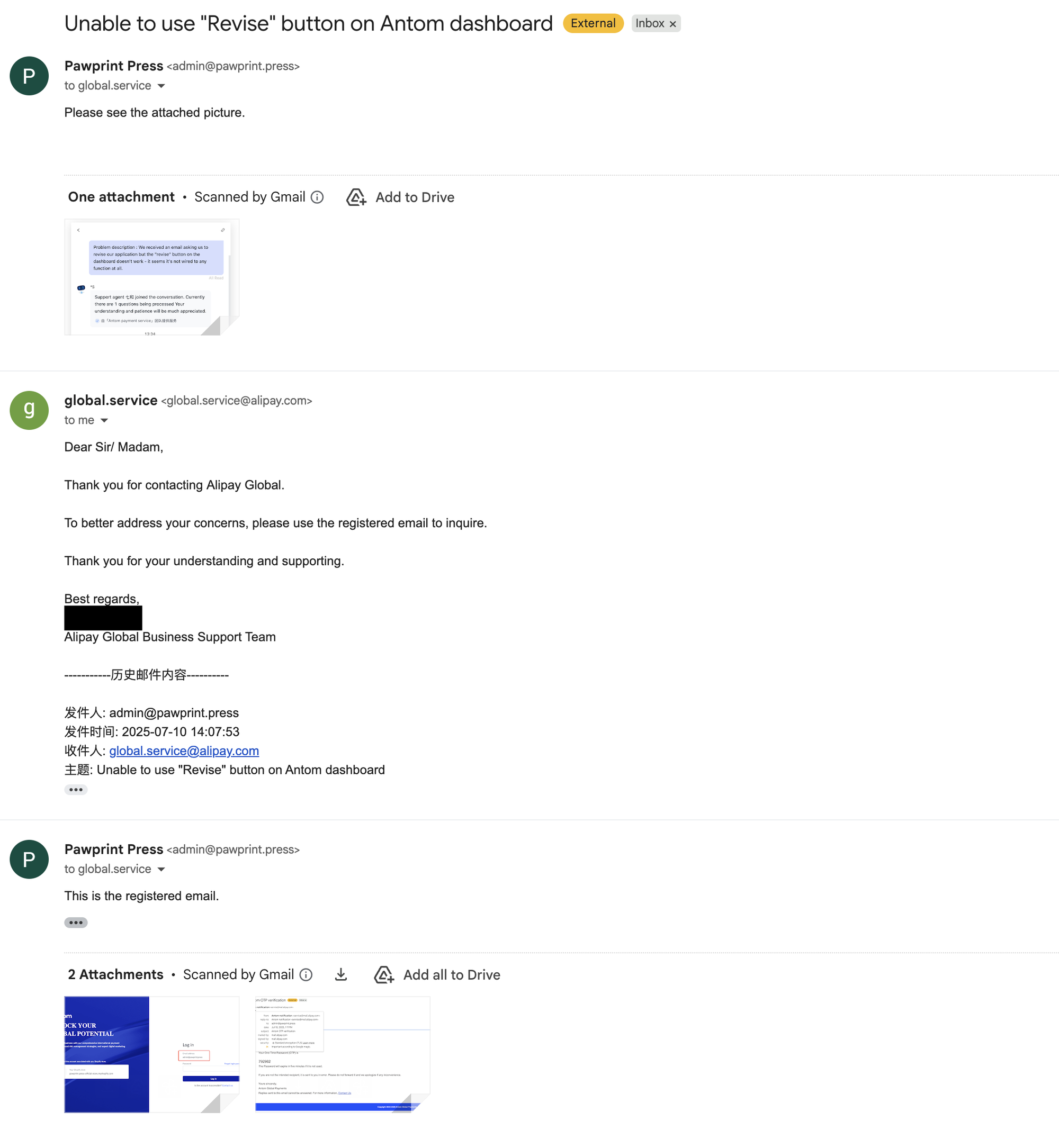

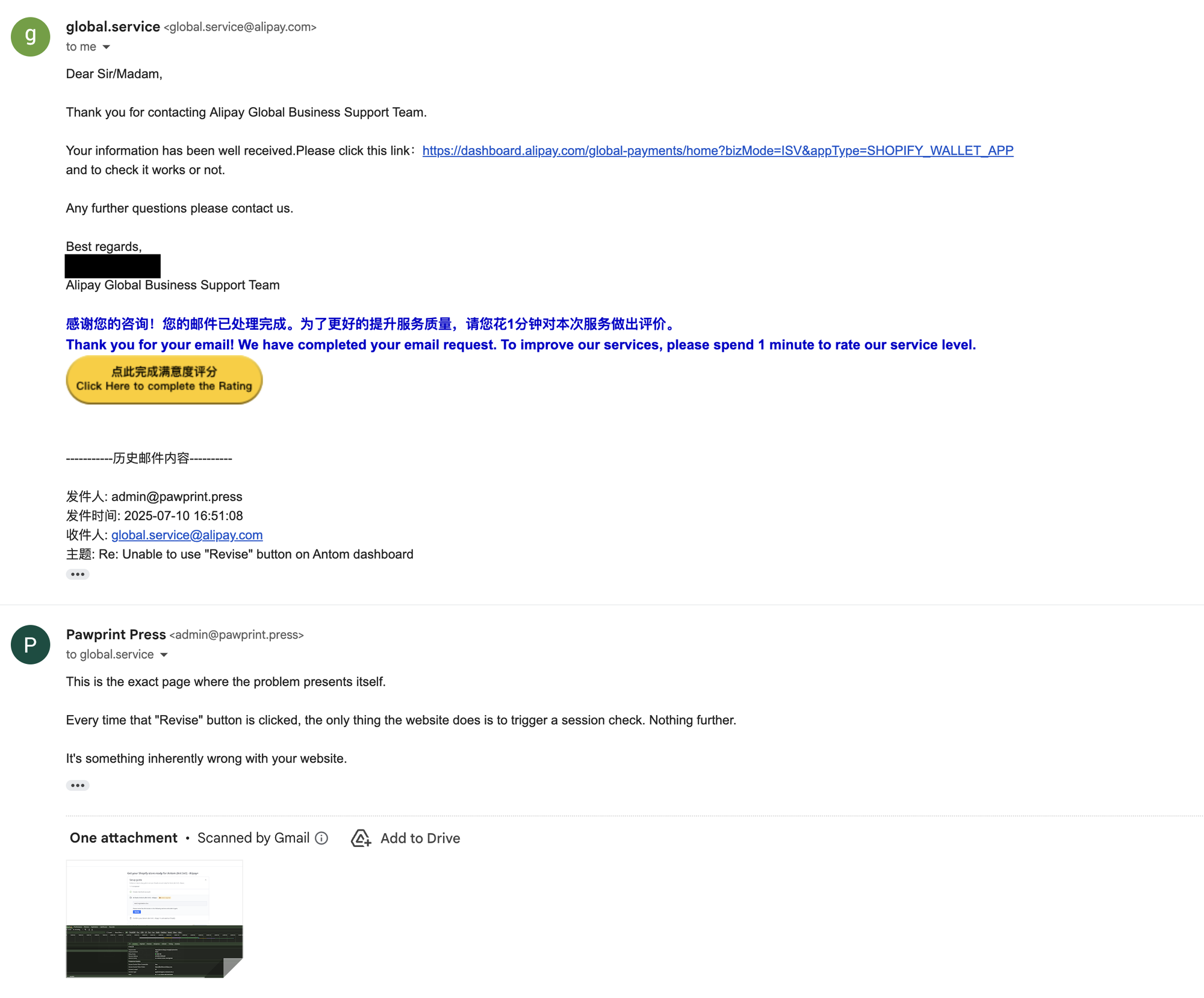

We first clicked the "Revise" button, hoping it would lead us to upload the documents they required. It didn't work. Upon inspecting the web page element, we found the button was not wired to anything at all. The only thing the button did was to trigger a session check.

We used the web chat module to seek help. Somebody appeared with their name partially redacted next to their avatar, even though the AI agent had already disclosed their full name in a notification message. A very classic information breach, but what's the point of redacting a nickname anyway? For those who don't know, Alibaba's founder, Jack Ma, is a huge fan of Chinese wuxia fiction, and he requires everybody at Alibaba to have a wuxia-style nickname. People there literally use these names at work.

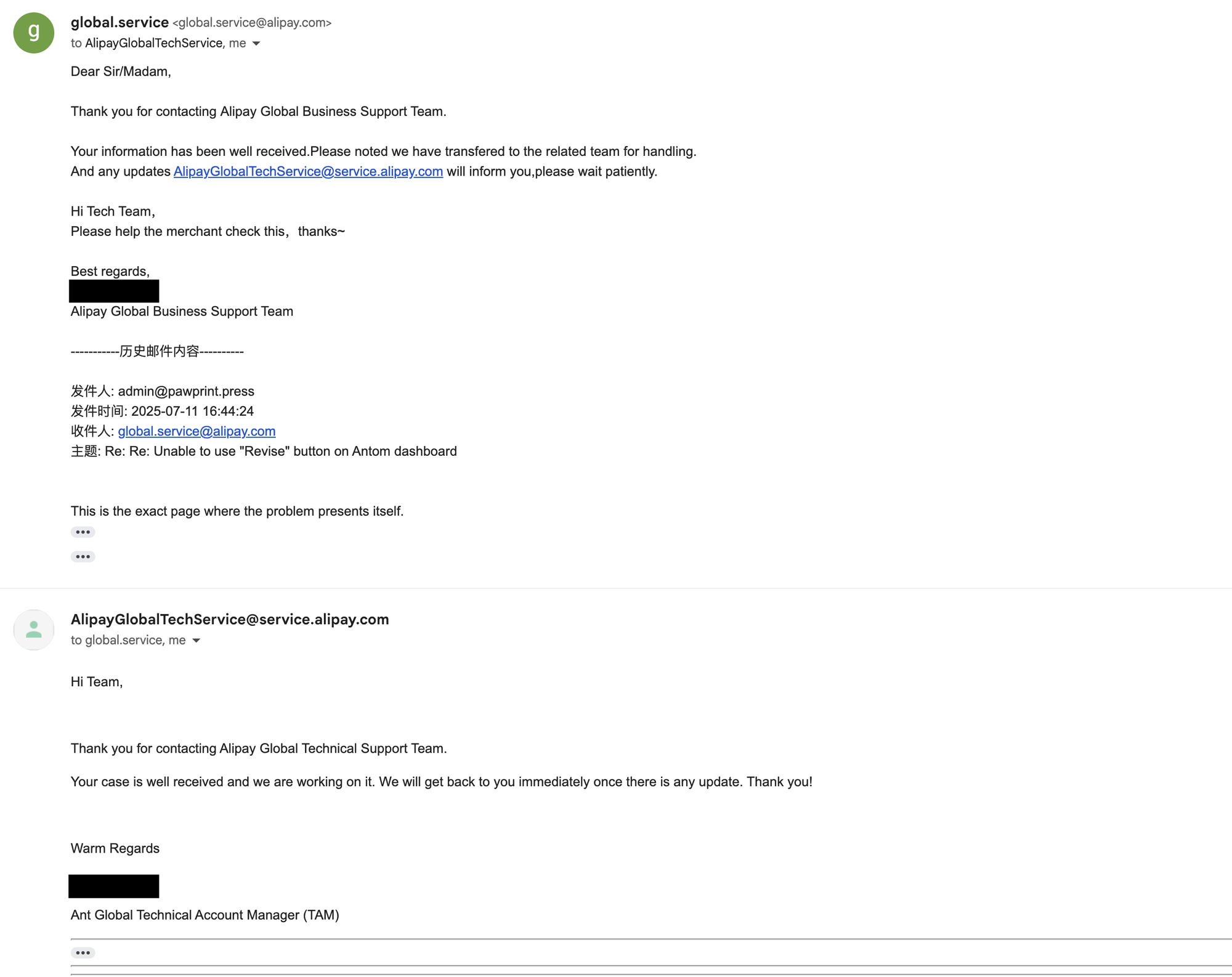

The guy was very straightforward. No polite shit talk. The first thing they said was, 'Can you take a screenshot of the dashboard?' We actually loved that; we initially thought it was a sign we were dealing with technical people instead of customer service. Then it turned out they were just untrained, as they simply referred us to an email address for what they called their 'international merchant service team'.

After a very short but desperate 'who's who' check, we were told to try that page again, but nothing changed. We had to teach them Website Development 101 once again, but luckily, this time they found the real technical team.

We were completely desperate when explaining Website 101 to a "business support team," but they did quickly send the ticket to tech. Good job on that part.

Finally, the button was fixed in four days, and we uploaded the documents. It also made us realize how infrequently this website was used, since if anyone else had encountered the same issue, they would have reported it to Antom and gotten it fixed. Or did they just give up? We can't imagine how many clients they have lost to their stupid programmers.

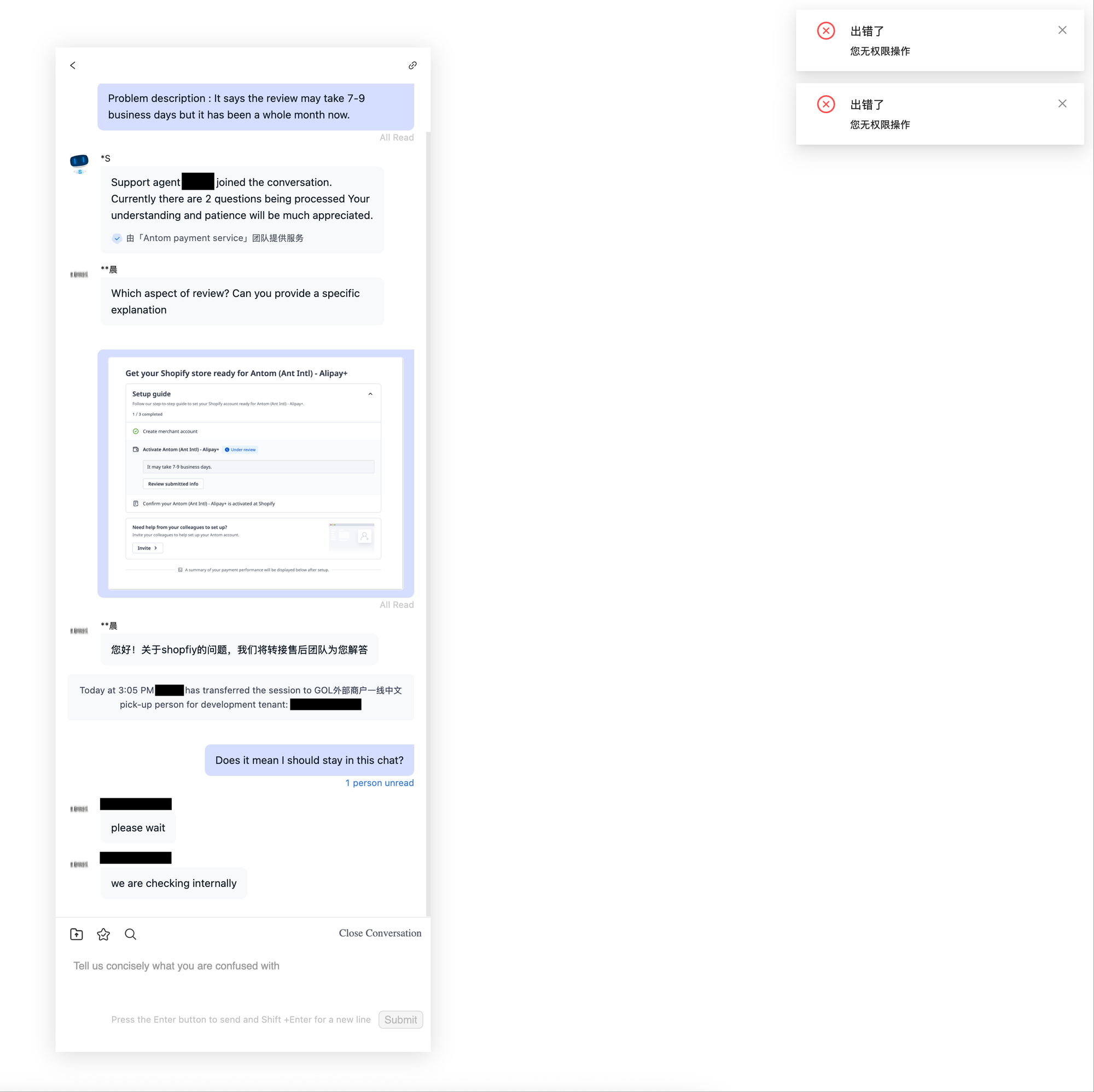

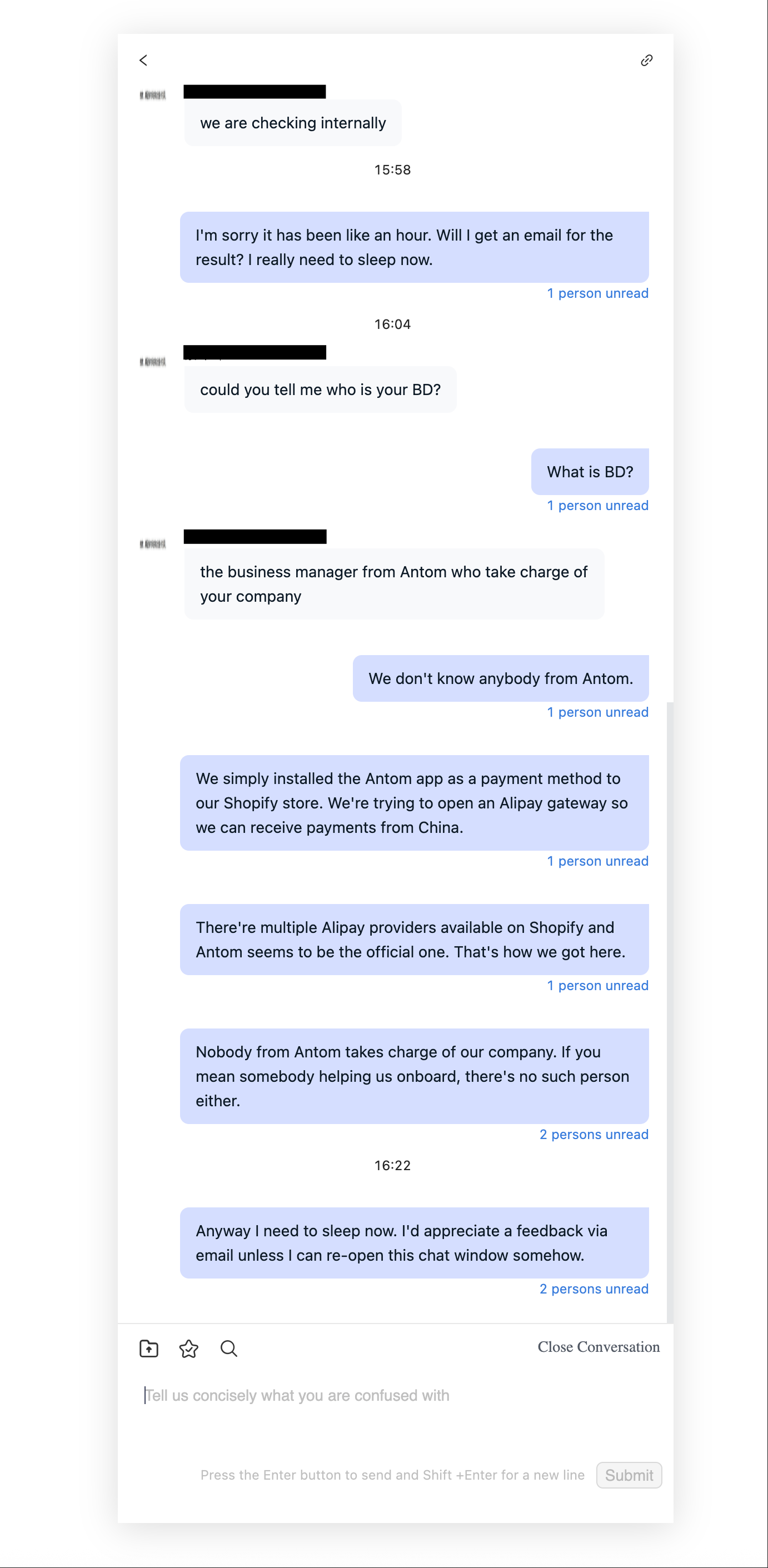

The confirmation page told us that it would usually take 7-9 days. We were patient enough, but after a whole month, we thought it was time to poke them. We went to the online chat module once again.

No idea how they have tampered with the online chat page since last time, because while the chat window remained functional, an error pop-up in the top-right corner kept displaying 'There's an error—You are not authorized to operate' in Chinese. Nevertheless, it didn't prevent us from communicating with the super dominant agent who ordered us to 'provide a specific explanation.'

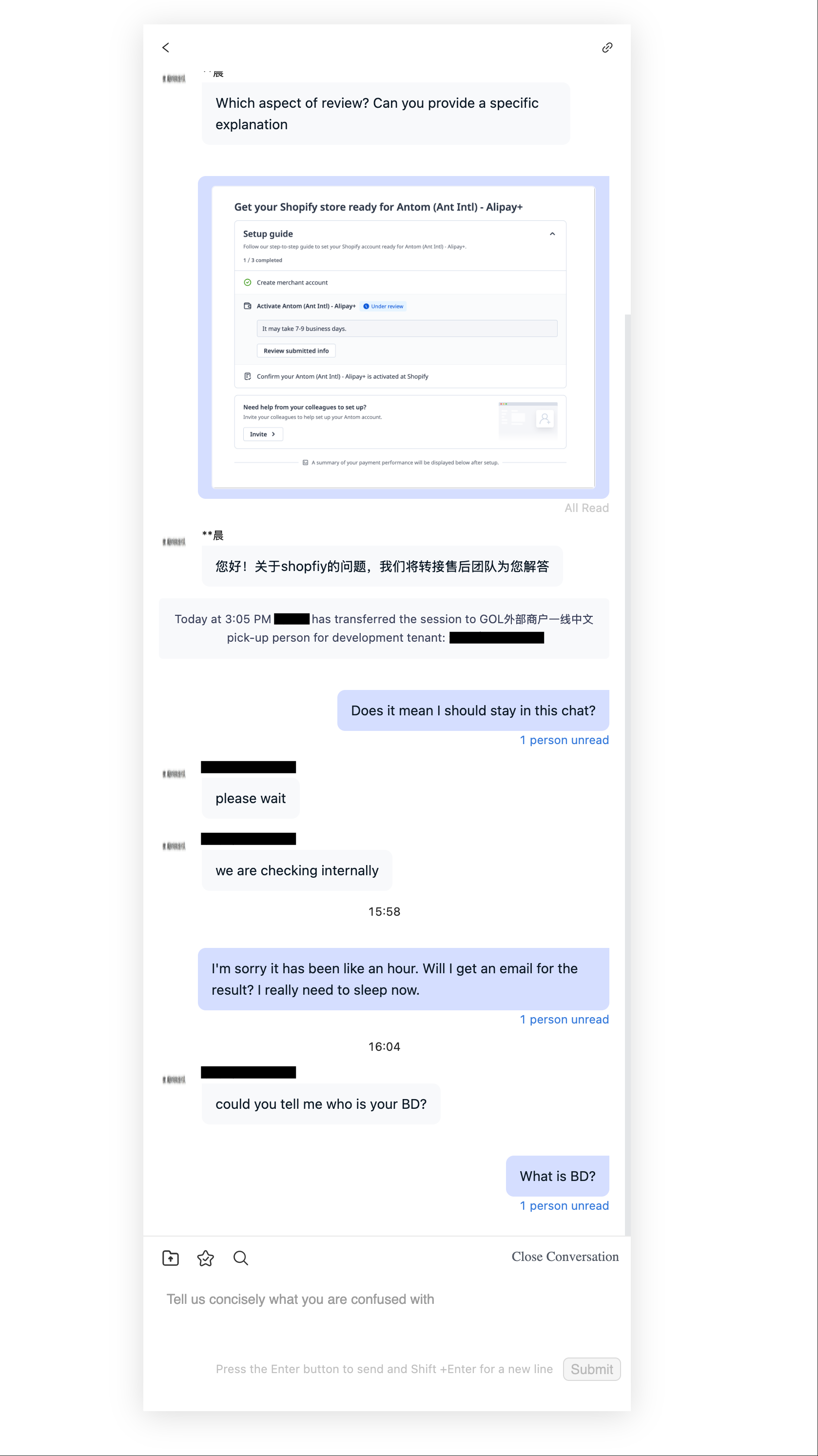

Once our screenshot was presented, the dom agent suddenly switched to Chinese and transferred us to another equally dominant agent who ordered us to wait when we asked if we should stay in the chat. We complied, but it was really late in our time zone, so we plucked up our courage to ask if we could just get the result via email.

After subjecting us to neglect play for an entire hour, the even more dom agent pushed the conversation further in a kinky direction—they asked us who our BD was. Well, it wouldn't have surprised us if this had suddenly turned into a full-blown BDSM chat, especially considering how dom they all were. We still Googled what 'BD' could refer to when it comes to a person, but it didn't help much.

In the end, it was revealed that "BD" refers to "Business Development," in the context of someone doing that job. Though, in their explanation, it's someone "who take charge of our company." We guess all of Alibaba is running under a dom culture.

This further revealed that nobody was actually using this Antom website (corroborating our aforementioned theory about the website bug). Apparently, Alibaba hired a bunch of field promotion staff ("BDs") to sell Alipay to international merchants. So, their customer service staff was under the impression that every client is associated with a BD; otherwise, they couldn't understand how the client even got there.

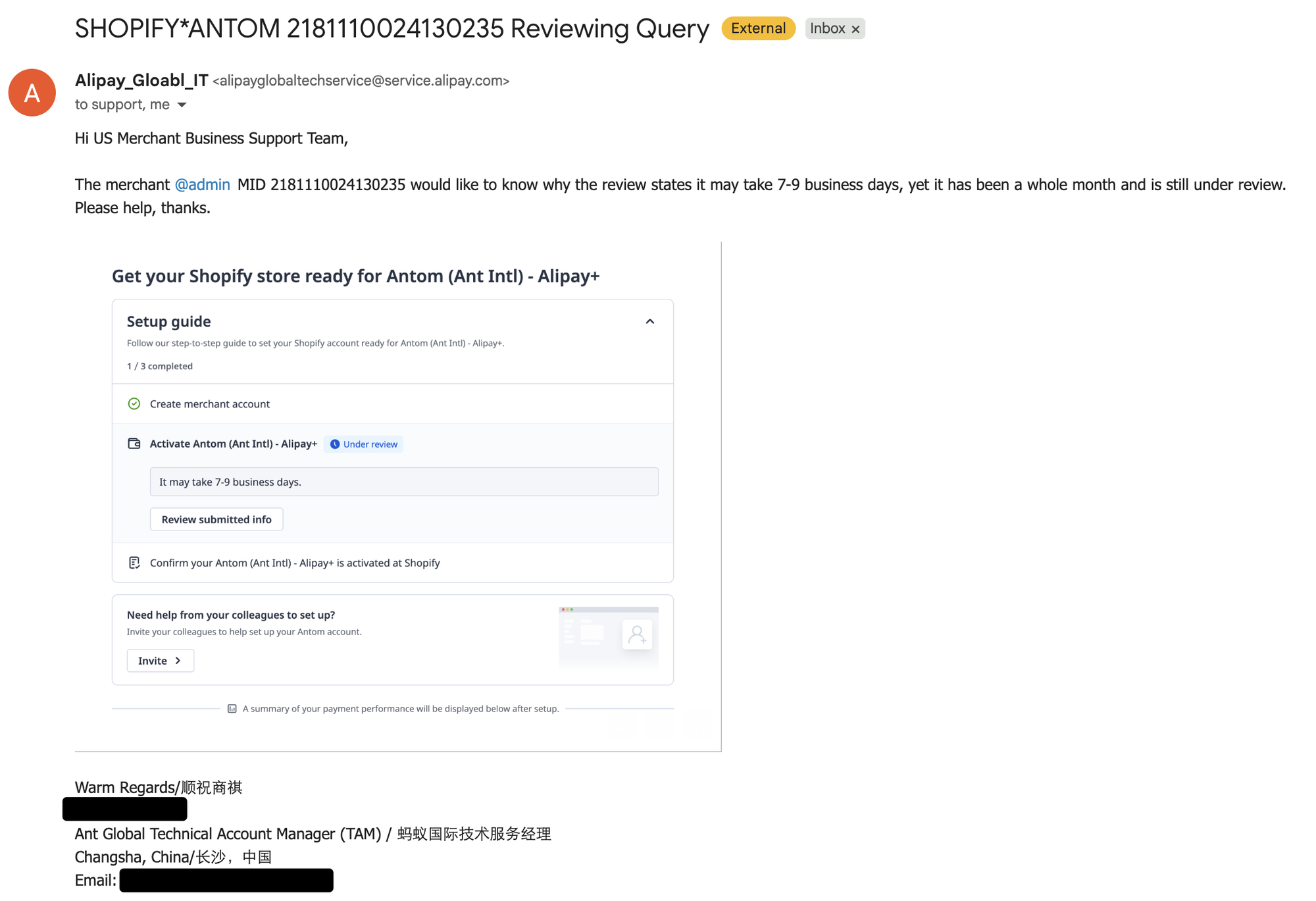

In the end, they were kind enough to send an email to their 'US Merchant Business Support Team.' On the same day, we received an automated email asking us to submit the exact same documents we had already submitted. And then, two months later, we got a new email with a link pointing to the exact same page, asking for the exact same documents we had already submitted twice.

Another three weeks later—nearly four months since we began the application—they sent us an email saying our application had been declined. No reason was given.

At this point, we simply concluded that we're tired of Alipay.

And we think you can now form your own judgment regarding the actual ability of the most leading, most advanced fintech company in China.

We have been fans of fintech ever since we started our business. Due to the nature of our business and our international team, many big banks see us as risky, poor people not worth their service. But fintech platforms have always been our friends. We are currently using Wise and Mercury (mainly Mercury nowadays), and they both offer a better experience than traditional banks (much like Alipay over Chinese banks, we imagine).

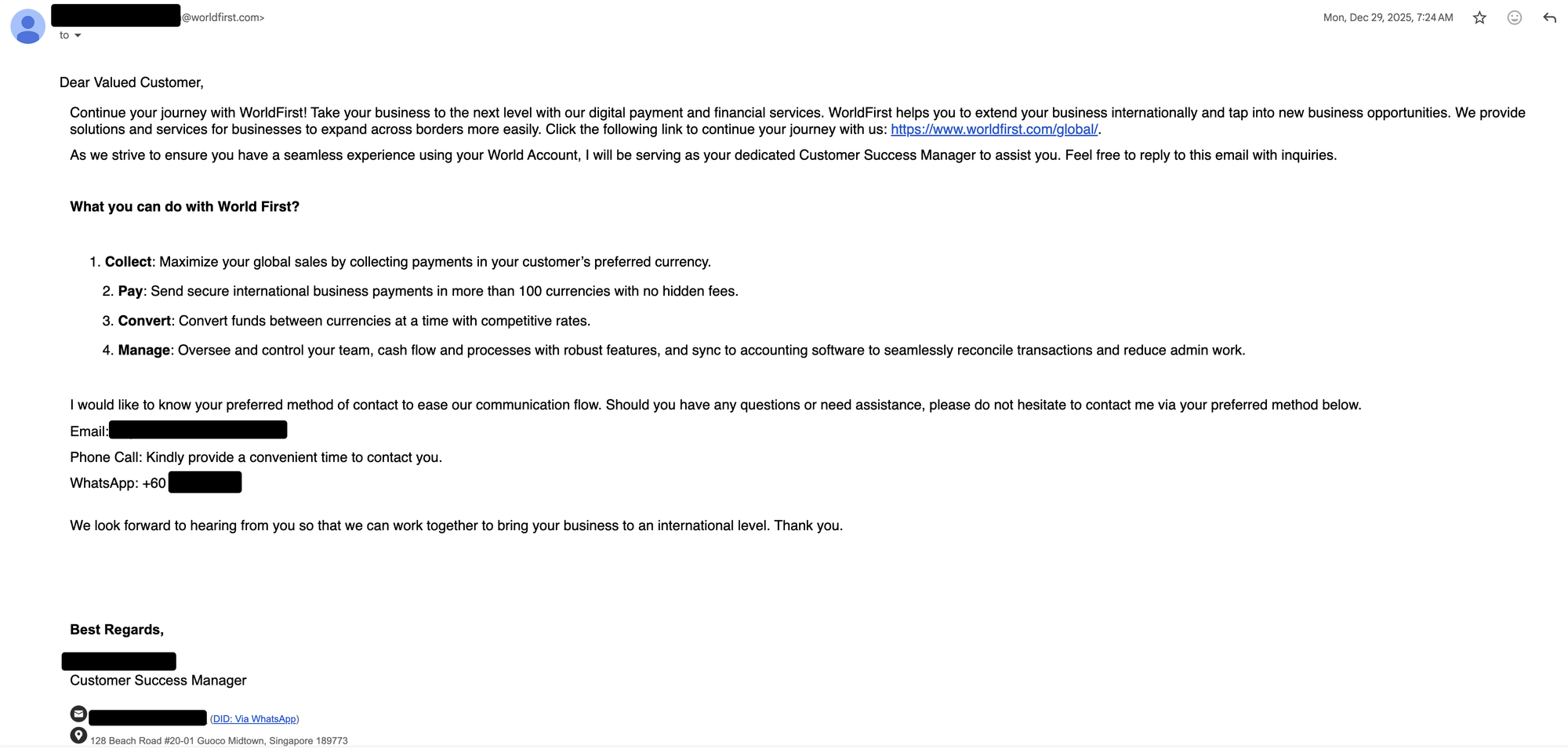

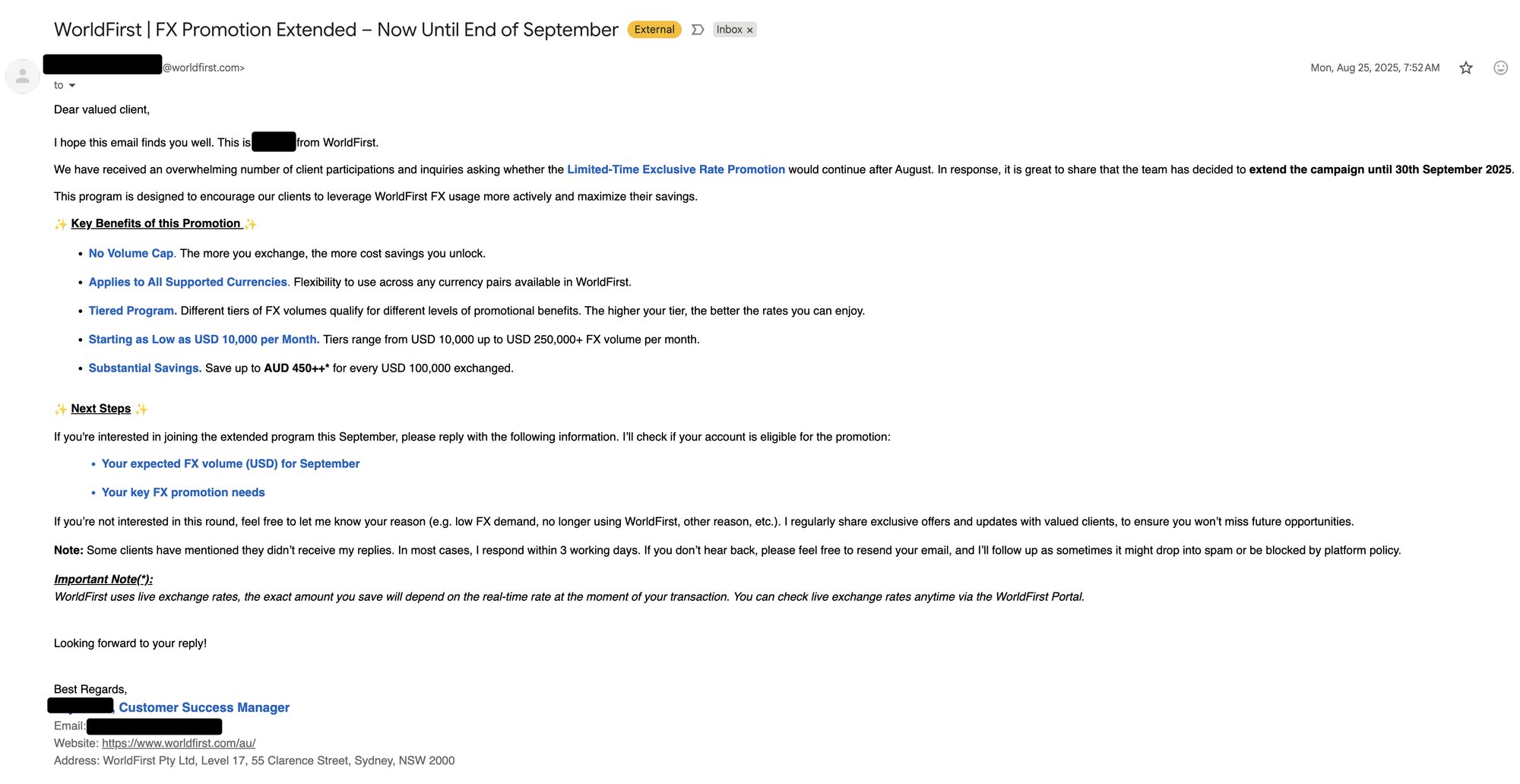

In our early years, we also used WorldFirst. The poor British platform was acquired by Alibaba, and we have been gradually ditching it ever since. The entire vibe of the platform became cheap and frivolous once Alibaba took over; it became more like a discount shopping platform (yep, we know what you really are, Alibaba) than a proper financial service. We also had to endure cold emails from various WorldFirst staff members.

All these kinds of shabby emails. Who would trust this kind of company to handle their money?

So, we are really eager to offer our Chinese friends a more convenient way to purchase from us; it’s just beyond our control. If someone can either find people at Alibaba (a BD?) to help us get this done, we’d much appreciate it. Or, if someone could just tell them to fire their entire imbecile Antom group.

Other than that, we just hope the current fintech platforms don't get acquired by Alibaba. Please, just leave us some sanity and a land of the free.